Global PV Equipment Market to Reach $43.8 billion by 2035: Report

China will remain the largest market for PV equipment even in 2035

March 31, 2026

Follow Mercom India on WhatsApp for exclusive updates on clean energy news and insights

The global solar industry is entering a decisive expansion phase, with photovoltaic (PV) manufacturing equipment investments projected to reach $250-$300 billion by 2035, and annual equipment spending is projected to rise from about $16.6 billion in 2025 to $43.8 billion by 2035.

This growth is driven by solar’s rapid cost decline and expanding deployment, with PV already supplying more than 10% of global electricity in 2024 and expected to become the lowest-cost source of electricity in almost all regions by 2030.

The European Photovoltaics Machinery and Equipment Study by Verband Deutscher Maschinen- und Anlagenbau (VDMA) highlights a structural imbalance where China dominates manufacturing across the silicon-based PV value chain, while Europe retains technological leadership but lacks the industrial scale and domestic market needed to compete effectively.

Solar’s Cost Advantage

The report identifies a fundamental shift in the global energy system, with solar PV moving from a niche technology to a central component of electricity supply. In 2024, solar generation exceeded 10% of global electricity consumption, reflecting sustained cost reductions and technological improvements.

Looking ahead, solar is expected to become the lowest-cost source of electricity in nearly all regions of the world by 2030. This cost competitiveness is driving strong growth in installations.

Annual global PV installations are projected to exceed 1 TW by 2028 and reach approximately 1.65 TW per year by 2035. Under the study’s medium scenario, the global PV market is expected to grow by approximately 2.5 times between 2025 and 2035.

PV Equipment Market Expands

The expansion of solar deployment is translating into significant growth in the PV manufacturing equipment sector. The report projects that the global PV equipment market will increase from approximately $16.6 billion annually in 2025 to $43.8 billion by 2035, with cumulative spending of $250 billion to $300 billion over the decade.

This growth follows a cyclical investment pattern described as the “Solarcoaster.” Periods of overinvestment and excess manufacturing capacity, sometimes reaching twice market demand, are followed by phases of consolidation and reduced capital expenditure, before investment rises again as transitions to new technology occur.

This cyclicality is also visible in materials manufacturing equipment. Investment is projected to decline from about $14.2 billion in 2024 to around $7.2 billion by 2028, then recover to approximately $21.8 billion by 2034.

Spending is concentrated in key equipment categories, including deposition systems, automation, ingot pulling, wet-chemical processing, thermal processes, and module assembly technologies such as stringers and laminators.

Technology Transition and Equipment Demand

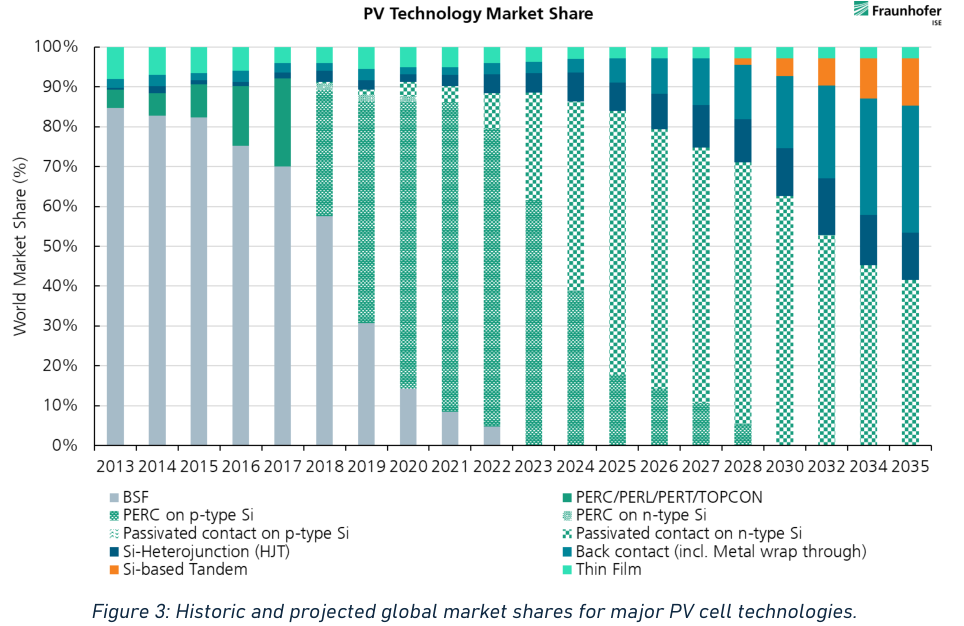

The report highlights a major transition in solar cell technologies. PERC technology is expected to be phased out by around 2030 and replaced by more efficient architectures, including TOPCon, heterojunction, and back-contact technologies. Together, these are expected to account for around 70% of the market and exceed 900 GWp of annual production by 2030.

In addition, silicon-based tandem technologies are expected to enter the market from around 2028. These transitions require changes to manufacturing processes and drive continued demand for new and upgraded equipment, even in a cyclical investment environment.

Manufacturing in Europe

Europe is a leader in PV manufacturing equipment technology, with companies recognized for engineering precision, advanced process control, and strong integration with research institutions.

However, the study highlights a significant gap between technological capability and industrial scale. Europe currently has limited manufacturing capacity, with approximately 9 GW of polysilicon capacity, 2.9 GW of solar cell production capacity, and 6.7 GW of module capacity, while ingot and wafer production is largely absent. Even under optimistic scenarios, module capacity is projected to reach about 44.6 GW by 2030, which remains modest relative to global demand.

European equipment is also associated with higher upfront capital costs, longer delivery times, and greater operational complexity. Survey findings indicate that while customers value European machines for quality, documentation, stability, and long-term performance, purchasing decisions are increasingly driven by cost, speed, and responsiveness.

The study also notes a perception gap: European manufacturers tend to rate themselves highly on performance metrics, while international customers place greater emphasis on cost efficiency and service responsiveness.

China’s Dominance

The study identifies China as the dominant force in global PV manufacturing. In 2024, Chinese companies accounted for 81% to 93% of global manufacturing capacity at major stages of the silicon-based PV value chain.

This dominance has been built through strong industrial policy support, integrated supply chains, and rapid scaling. The report notes that Chinese manufacturers now source virtually all PV equipment domestically, supported by extensive state backing and a mature industrial ecosystem.

China remains the largest market for PV equipment, with annual capital expenditure projected to increase from approximately $13.3 billion in 2025 to $21.9 billion by 2035.

India’s Rapid Growth

India is identified as one of the fastest-growing markets for PV manufacturing and equipment demand. Annual PV equipment CAPEX is projected to increase from around $0.5 billion in 2025 to approximately $7.5 billion by 2035.

This growth is driven by strong policy frameworks, particularly the Production-Linked Incentive (PLI) program, which supports domestic manufacturing across the solar value chain. The report identifies India, along with the U.S., as a key destination for PV equipment exports.

The study also indicates that the localization of upstream materials is expected to expand in India over the next three to six years. However, this transition faces challenges due to high capital requirements and the energy-intensive nature of upstream manufacturing, particularly in glass and polysilicon.

India added nearly 119 GW of solar modules and over 9 GW of solar cell capacity in 2025, according to Mercom India’s State of Solar PV Manufacturing in India 2026 report. The country’s cumulative module manufacturing capacity reached approximately 210 GW, while cumulative cell capacity stood at roughly 27 GW by December 2025.

U.S. a Growth Market

The U.S. is another major growth market, with PV equipment CAPEX projected to rise from approximately $800 million in 2025 to around $4.9 billion by 2035. This expansion is driven by policy incentives under the Inflation Reduction Act (IRA), which has created strong momentum for domestic manufacturing.

The report highlights that both India and the U.S. have become primary markets for European equipment suppliers, reflecting a shift in global demand away from China.

Southeast Asia

Southeast Asia continues to play an important role in global PV manufacturing, with annual equipment spending projected to increase from about $1.4 billion in 2025 to $3.2 billion by 2035. Outside China, manufacturing remains concentrated in East Asia, often involving affiliates of Chinese producers.

Other regions, including the Middle East and North Africa, are also expected to see growth in manufacturing capacity, supported by policy initiatives, although on a smaller scale.

Supply Chain Constraints

The report highlights the critical role of raw materials in PV manufacturing. Materials such as glass, aluminum frames, encapsulants, and silver paste together account for approximately 80% of total material expenditure.

Establishing local production for these materials is complex, with setup times typically ranging from 3 to 6 years, depending on the segment. Capital expenditure requirements vary significantly, with glass manufacturing costs approximately $30–40 million per GW of capacity, while polysilicon production costs around $10–14 million per GW.

China has achieved high levels of localization across these upstream segments, while other regions continue to face challenges related to cost, energy intensity, and supply chain development.

Turnkey Solutions and Financing Challenges

The report identifies growing demand for turnkey manufacturing solutions, particularly in emerging markets such as India and the U.S. These solutions involve delivering complete production lines rather than individual machines.

However, European suppliers often face challenges in providing turnkey offerings due to financial risks associated with performance guarantees and project delivery. The study suggests that overcoming this barrier will require new business models, including partnerships, risk-sharing mechanisms, and stronger support through export financing and public guarantees.

The study concludes that the global PV equipment market represents a major economic opportunity, driven by rapid solar deployment and ongoing technology transitions. However, it also highlights increasing competition and structural imbalances.

While Europe remains a global technology leader, its future competitiveness will depend on its ability to translate innovation into industrial scale. This will require building a domestic manufacturing base, strengthening policy coordination, and adapting to a global market increasingly shaped by cost efficiency, speed, and policy-driven expansion.

Arjun Joshi

More articles from Arjun Joshi.