Australia Weighs $2.5 Billion Polysilicon Facility in New South Wales

ARENA estimates the proposed facility can support the manufacture of 27 GW solar modules annually

June 4, 2026

Follow Mercom India on WhatsApp for exclusive updates on clean energy news and insights

Australia is assessing the potential development of a 50,000-ton-per-year solar-grade polysilicon facility at the Hunter Energy Hub in New South Wales, according to a study supported by the Australian Renewable Energy Agency (ARENA).

According to the report, the proposed facility in Australia could produce 50,000 tons of ultra-pure polysilicon annually, enough to support about 27 GW of solar module manufacturing. It said a large-scale polysilicon facility could serve as an anchor industry for a broader domestic solar manufacturing ecosystem covering quartz, metallurgical silicon, wafers, cells, and modules.

The facility would require capital expenditure of AUD2.5 billion (~$1.8 billion) to AUD3.5 billion (~$2.5 billion). It would consume about 2.5 TWh to 3 TWh of electricity annually, equivalent to more than 1% of the total National Electricity Market supply.

The facility would operate at a continuous load of about 300 MW to 350 MW.

The study examines the potential for establishing polysilicon production in Australia, with a focus on the Hunter Energy Hub. It assesses global market dynamics, supply chain constraints, Australia’s strategic position, and the technical, economic, and regulatory factors that could influence project viability.

The proposed facility would support Australia’s efforts to participate in diversified global solar supply chains and develop exports beyond coal and liquefied natural gas.

Demand for Non-Chinese Polysilicon

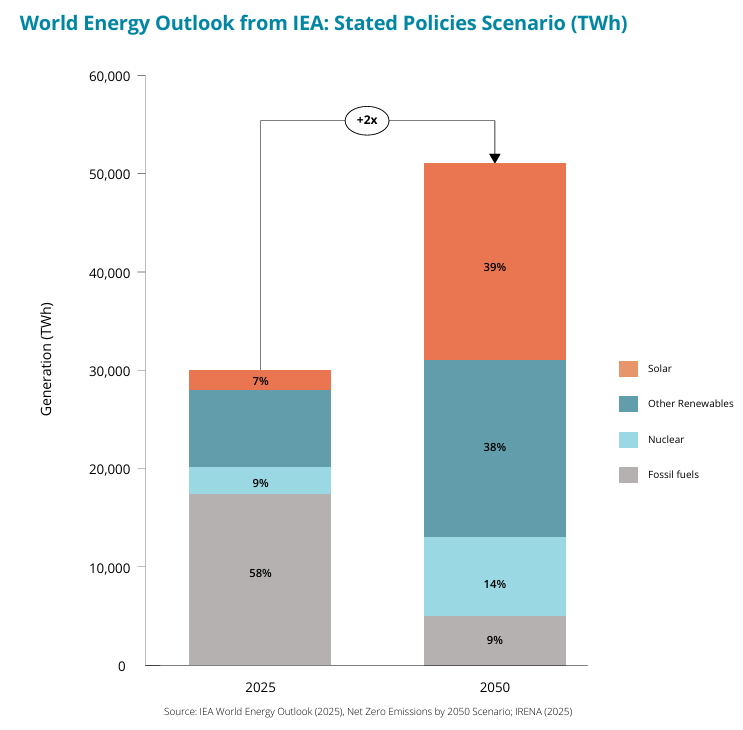

The study is based on expectations that global solar deployment will continue to expand. It projects solar power’s share of global electricity generation to increase from about 7% in 2025 to 39% by 2050, while coal declines from 38% to 8%, and gas falls from 22% to 13%.

Annual global solar demand is forecast to reach 1.2 TW to 1.7 TW by 2030. Polysilicon demand is estimated at 1.9 million tons to 2.7 million tons.

The study notes that solar generation costs have fallen by 88% since 2010 to around $0.04/kWh in 2025, compared with about $0.08/kWh for fossil-fuel generation.

A key driver for the proposed project is the expected shortage of non-Chinese polysilicon. China accounted for about 95% of global polysilicon production and had around 3.5 million tons of capacity in 2025, compared with demand of about 1.2 million tons. The report says this created oversupply and pushed prices below $10/kg.

According to the report, the solar-grade polysilicon supply outside China was estimated at only 69,000 tons in 2025, despite a total non-Chinese capacity of about 199,000 tons, because much of that capacity serves electronic-grade markets. It is projected that demand for non-Chinese polysilicon could exceed available supply by about 240,000 tons by 2035 and more than 350,000 tons by 2040.

In February this year, the U.S. decided to retain antidumping duties on polysilicon imports from China and Taiwan. The U.S. move came close on the heels of China’s decision to extend the imposition of antidumping duties on imported U.S. solar-grade polysilicon for five years, effective January 14, 2026

The report also projects a shift in solar demand growth. China’s share of global photovoltaic demand is expected to decline from 56% in 2025 to 18% by 2050. India’s share is expected to rise from 5% to 23%, while the rest of the world’s share is projected to increase from 22% to 47%.

Technology and Policy Support

The study identifies the Siemens process as the dominant technology for producing high-purity solar-grade polysilicon. The process accounted for about 90% of global solar polysilicon production in 2024 and is expected to retain about 80% market share by 2030.

The process requires about 55 kWh of electricity per kilogram of silicon. For a 50,000-ton facility, this would equal about 2.7 TWh of electricity annually.

Production involves hydrochlorination, trichlorosilane purification, chemical vapor deposition, chlorosilane recovery, and recycling systems.

The proposed facility would also include on-site chloralkali production and chemical recovery systems to achieve near-zero liquid waste discharge through material recovery and closed-loop process integration.

The study identifies the fluidized bed reactor process as the only significant alternative technology at a commercial scale. The process reduces water consumption by about 30% compared with the Siemens process but requires about three times as much steam. It is expected to account for about 20% of the market share by 2030.

Costs

The base case assumes an upfront grant of AUD1 billion (~$718 million) to AUD1.5 billion (~$1.1 billion) and production credits of about AUD200 million (~$144 million) annually for 10 years.

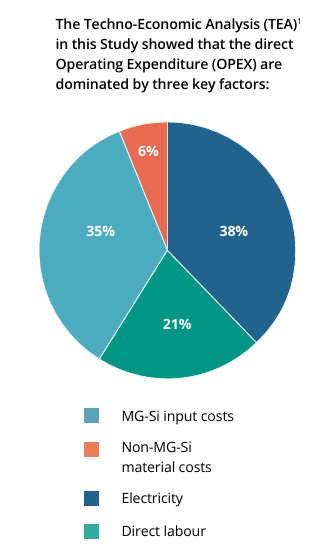

Electricity accounts for 38% of operating expenditure, followed by metallurgical silicon feedstock at 35%, labor at 21%, and other materials at 6%.

The study identifies electricity prices and polysilicon sales prices as the most significant determinants of project viability. It estimates that Australian construction costs are two to three times higher than those for comparable Chinese projects. Long-term access to competitive supplies of electricity and metallurgical silicon would remain critical.

Advancing to a Front-End Engineering Design study would cost AUD20 million (~$14.4 million) to AUD30 million (~$21.5 million) over 18 to 24 months. The study would refine costs, assess commercial assumptions, address major risks, and support a potential future financial investment decision.

Meghana Prasad

More articles from Meghana Prasad.